Quick Sellers: Knowledgeable Liquidity Suppliers

Quick sellers typically have a foul repute, seen as market disruptors who revenue from declining costs. But, they play a vital function in making markets extra environment friendly by figuring out overvalued belongings and correcting mispricings. A latest research uncovers one other shocking side of their habits: relatively than simply demanding liquidity, essentially the most knowledgeable quick sellers really present it. Utilizing transaction-level information, the analysis exhibits that these merchants provide liquidity, particularly on information days and when buying and selling on recognized anomalies, difficult the traditional view of quick sellers as merely aggressive market individuals.

For an extraordinary particular person, investing has the prospect of shopping for regular and financially sound firms that are likely to do effectively sooner or later, return their shareholders a part of the revenue, and thus profit them within the long-term with compounding returns and complete society with the moral allocation of capital for enhancing the world. With the appearance of ETFs (exchange-traded funds), buying firms’ baskets grouped on numerous metrics based mostly on typical indicators and indicators similar to regional or nation location or similar or comparable trade sectors is feasible, which makes diversification even simpler.

However, short-selling is a promising and profitable endeavor that pulls risk-seeking merchants, typically inexperienced, who get burnt by not understanding the prospect of liquidity provide and demand mechanics. There are numerous eventualities and examples from the historical past of painful quick squeezes (Volkswagen and GameStop) that made, at that second, the correct aspect worthwhile and rich, and, on the opposite aspect, limits-to-arbitrage eventualities the place you, even if you happen to needed to both cowl your quick or purchase wrongly valued asset, simply couldn’t as a result of there have been no shares to acquire. Invoice Ackman shorting Herbalife, different activist buyers, or a neverending myriad of Tesla shorters know their tales. Nevertheless, there are additionally short-only hedge funds specializing in, for instance, deep delve into Phases I, II, and III of scientific trials and/or fairly guess on not clearing FDA drug approval and might estimate failure charges to the extent that they will, based mostly on an informed guess, take quick positions on biotechs which might be probably not to achieve the long term.

Exhausting to argue that short-sellers are a significant a part of free markets, which contribute to cost discovery and the convergence course of to correct asset pricing valuations. Not surprisingly, such a feat, which incorporates limitless losses (you finally as soon as must cowl your quick positions), is warned towards the extraordinary investor, and knowledgeable buying and selling carried out by skilled buyers has a bonus at their ft.

At this time, we confront frequent preconceptions in regards to the short-selling with an fascinating analysis paper that offers honoring nods towards short-sellers: Basically, the summary states that essentially the most skilled quick sellers act as liquidity suppliers relatively than takers, which is a novel level that casts quick sellers in a extra favorable gentle. However, contributing to raised value discovery by supplying higher bid-ask spreads (posting and sustaining a vigorous order e-book, not aggressively hitting the market orders) helps extraordinary buyers set up or get out of their place at favorable costs than in different illiquid environments.

By distinguishing between liquidity-supplying and liquidity-demanding quick gross sales, analysis paper challenges the traditional knowledge that solely these demanding liquidity are knowledgeable. Liquidity-supplying quick sellers are, in actual fact, higher at predicting future inventory returns, notably over extra prolonged holding durations. The research aligns with latest theoretical work that posits a twin function for knowledgeable merchants, together with liquidity provision to capitalize on long-lived data. The truth that the identical quick sellers provide liquidity and enhance market effectivity provides to an already difficult activity for regulators.

Stealthy Shorts: Knowledgeable Liquidity Provide paper exhibits that quick sellers who commerce within the course of their data, which presumably impacts costs, accomplish that by liquidity-providing trades. The outcomes, which present they’re the identical, add to the problem confronted by regulators who wish to stop hostile value actions whereas guaranteeing that markets are as liquid as potential, particularly in instances of disaster.

The paper begins the evaluation by replicating a well-documented sample within the cross-section of inventory returns: shares with a excessive quick sale quantity relative to their complete buying and selling quantity underperform these with a low shot quantity ratio). Extra importantly, authors uncover fascinating heterogeneous patterns when decomposing this ratio into liquidity-supplying quick quantity ratio (LSS) and liquidity-demanding quick quantity ratio (LDS). Opposite to standard knowledge, their portfolio evaluation exhibits that solely LSS negatively predicts future fairness returns.

Specifically, shares within the highest LSS quintile underperform these within the lowest quintile by a risk-adjusted return of 38 foundation factors over a 21-day holding interval. In distinction, the predictive energy of LDS over the identical holding interval is way weaker at simply 12 foundation factors, which is statistically indistinguishable from zero and pushed fully by the return on the day after portfolio formation. Cross-sectional regressions present that the return predictability related to LSS just isn’t subsumed when controlling for different well-known short-selling metrics and commonplace return predictors.

This implies that liquidity-supplying quick gross sales include distinctive details about future inventory returns. In extra checks, authors discover that documented predictability is neither concentrated in shares with particular traits nor pushed by explicit durations or samples of shares, and it holds for numerous various holding durations. Ultimate outcomes point out robust predictability of future returns from liquidity-supplying quick gross sales. In distinction, such predictability is absent for liquidity-demanding quick gross sales over holding durations longer than sooner or later. Liquidity-supplying quick gross sales could signify knowledgeable buying and selling by quick sellers with comparatively long-lived data.

Authors: Amit Goyal, Adam V. Reed, Esad Smajlbegovic, and Amar Soebhag

Title: Stealthy Shorts: Knowledgeable Liquidity Provide

Hyperlink: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4941397

Summary:

Quick sellers are extensively recognized to learn, which might usually counsel that they demand liquidity. We get hold of complete transaction-level information to decompose each day quick quantity into liquidity-demanding and liquidity-supplying elements. Opposite to standard knowledge, we present that essentially the most knowledgeable quick sellers are literally liquidity suppliers, not liquidity demanders. They’re notably informative about future returns on information days and commerce on distinguished cross-sectional return anomalies. Our evaluation means that market making and opportunistic risk-bearing are unlikely to elucidate these findings. As an alternative, our outcomes align with latest market microstructure idea, pointing to strategic liquidity provision by knowledgeable merchants.

As at all times, we current a number of thrilling figures and tables:

Notable quotations from the tutorial analysis paper:

“[Authors] shed additional gentle on the character of the return predictability and its hyperlink to the informational benefit inherent in liquidity-supplying quick gross sales. First, we use a framework much like that of Engelberg, Reed, and Ringgenberg (2012), and study the predictive energy of LSS for inventory returns round firm-specific information launch days. If the predictive means of liquidity-supplying quick gross sales stems from an informational benefit, then LSS ought to predict returns notably on these days when information is launched and data is included into inventory costs. In step with this speculation, we discover that liquiditysupplying quick gross sales are notably informative about future returns on information days in comparison with non-news days. Moreover, as with our decomposition methodology, we reveal that this elevated predictive energy is current completely within the residual element of LSS, additional supporting the notion that liquidity-supplying shorts are, on common, knowledgeable about firm fundamentals.

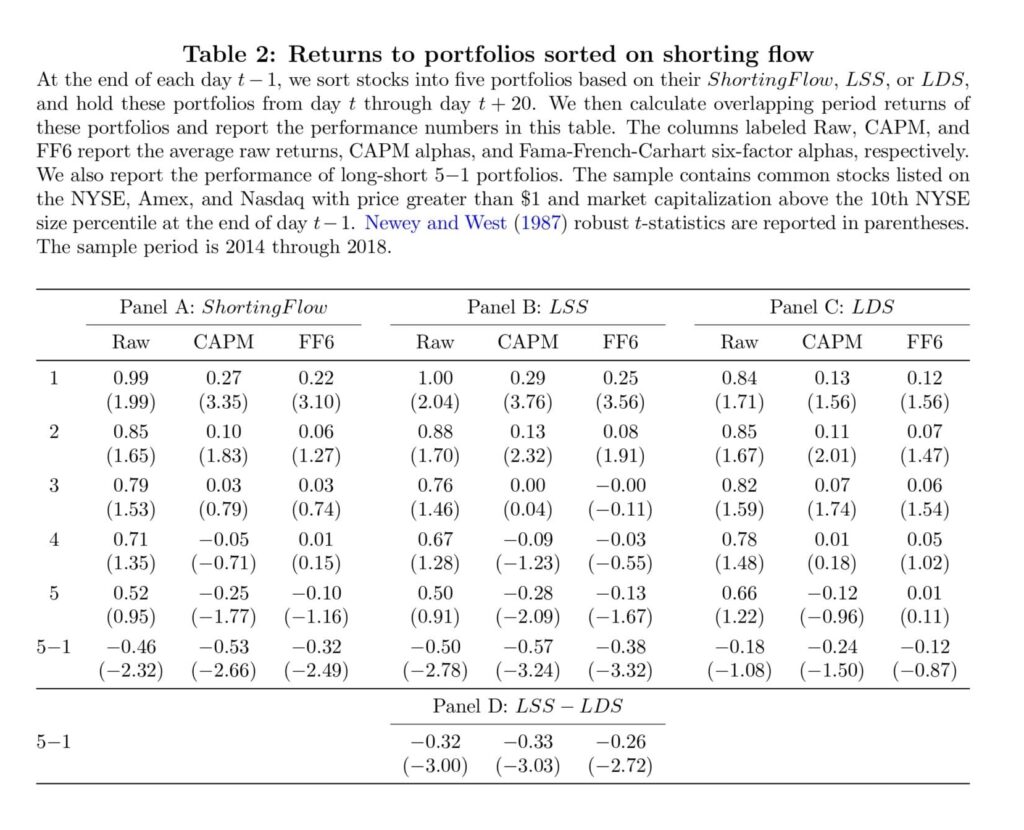

[Authors] report cumulative six-factor alphas for unfold portfolios shaped based mostly on kinds of LSS or LDS for future horizons various from 1 by 21 days in Determine 2. In step with prior literature (see, e.g., Boehmer, Jones, and Zhang, 2008 and Engelberg, Reed, and Ringgenberg, 2012), we discover that each LSS and LDS considerably and negatively predict subsequent day t return, with each day six-factor alphas of round 0.10%. Growing the holding interval, we discover that the predictive energy of LDS weakens, with no statistically vital predictability after seven days. In distinction, we discover that LSS is a powerful destructive predictor of future fairness returns throughout all holding durations starting from 1 by 21 days. For a 21-day holding interval, the unfold portfolio based mostly on LSS has a cumulative six-factor alpha of just about 0.40%. Thus, this determine paperwork a putting empirical sample: liquidity-supplying shorts negatively predict future fairness returns, whereas liquidity-demanding shorts don’t, at the least for horizons of longer than per week.We current returns and alphas on quintile portfolios and the unfold portfolio for a horizon of 21 days in Desk 2. Panels A, B, and C kind on complete ShortingF low, LSS, and LDS, respectively. Panel A exhibits that closely shorted shares underperform evenly shorted shares. This discovering is strong whether or not we take a look at uncooked returns or risk-adjusted returns and is statistically vital with t-statistics starting from −2.32 to −2.66. In step with prior literature (see, e.g., Boehmer, Jones, and Zhang, 2008), we discover that the efficiency distinction between portfolios 1 and 5 is pushed primarily by the outperformance of quintile 1 relatively than by the underperformance of quintile 5.

[Authors] discover that, with hardly any exceptions, the coefficient on LSS is destructive and statistically vital whereas that on LDS is statistically insignificantly completely different from zero.13 The outcomes are comparable throughout two subsamples (rows (2) and (3)), for various filters on shares (rows (4) by (6)) and for various horizons of future returns (rows (7) by (9)). Row (9) specifically exhibits that the predictability extends to 40 days. Thus our outcomes usually are not pushed by particular time durations, particular samples of shares, or explicit calculations of variables.General, the outcomes of this part present a powerful predictability of future returns related to liquidity-supplying quick gross sales however the absence of such predictability related to liquidity-demanding quick gross sales. These outcomes counsel that liquidity-supplying quick gross sales could signify knowledgeable buying and selling from buyers with comparatively long-lived data.

[R]esults [] point out that the predictive energy of quick gross sales for the cross-section of fairness returns stems from knowledgeable liquidity provision by quick sellers. Furthermore, the graphical illustration of the return predictability for various holding durations in Determine 2 means that these quick gross sales commerce on data that’s slowly included into inventory costs.”

Are you on the lookout for extra methods to examine? Join our e-newsletter or go to our Weblog or Screener.

Do you wish to be taught extra about Quantpedia Premium service? Examine how Quantpedia works, our mission and Premium pricing provide.

Do you wish to be taught extra about Quantpedia Professional service? Examine its description, watch movies, assessment reporting capabilities and go to our pricing provide.

Are you on the lookout for historic information or backtesting platforms? Examine our checklist of Algo Buying and selling Reductions.

Or comply with us on:

Fb Group, Fb Web page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookConsult with a buddy

, Alibaba Gr Hldgs (OTC:BABAF)")