If a dealer needs to provoke an at-the-money non-directional butterfly, what distinction would it not make if the fly had wider or narrower wings?

Contents

Effectively, let’s check out each on the SPX index.

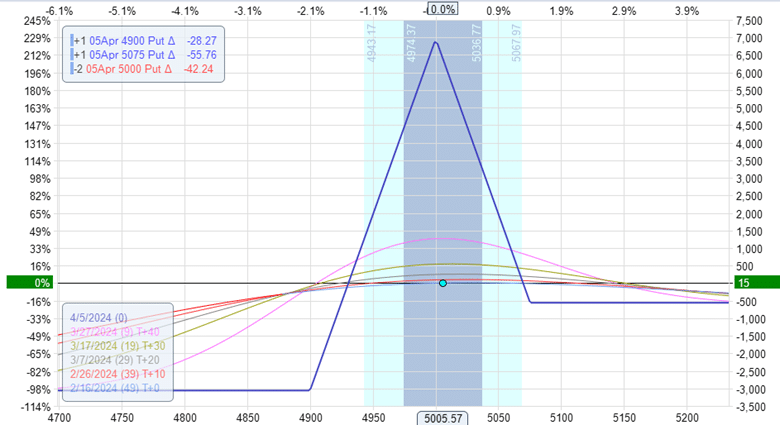

First, contemplate a wider fly with an higher wing width of 75 factors and a decrease wing width of 100 factors.

Date: February 16, 2024

Worth: SPX @ 5005

Purchase one April 5 SPX 4900 put

Promote two April 5 SPX 5000 put

Purchase one April 5 SPX 5075 put

Debit: -$560

The max danger is $3060, and the theoretical max revenue is about $7000, as proven within the payoff graph under.

This provides a reward-to-risk of two.3.

The Greeks are:

Delta: 0.52

Gamma: -0.03

Theta: 7.35

Vega: -93.42

Theta/Delta: 14.2

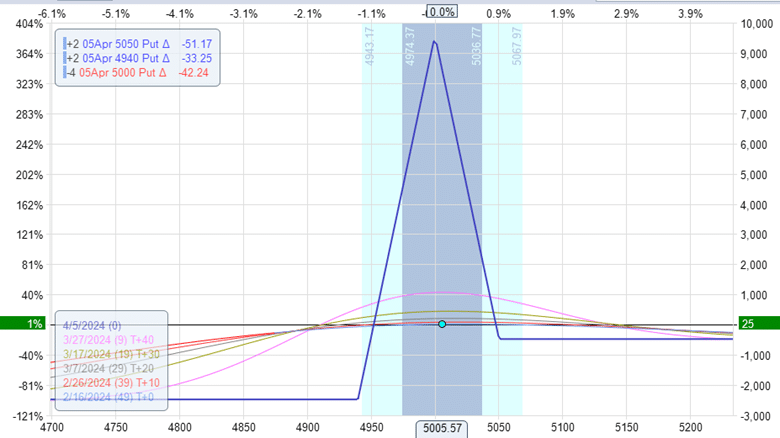

Now contemplate a narrower fly with 50/60 higher and decrease wing widths.

Date: February 16, 2024

Worth: SPX @ $5005

Purchase two April 5 SPX 4940 put

Promote 4 April 5 SPX 5000 put

Purchase two April 5 SPX 5050 put

Debit: -$480

We’re utilizing two contracts right here to get the capital utilization of the slender fly to be virtually corresponding to the capital utilization of the extensive fly.

Whereas the reward-to-risk ratio and the ratio between the Greeks is not going to change based mostly on the variety of contracts, absolutely the worth of the Greeks is cumulative relying on the variety of contracts.

This may make it a fairer comparability.

With two contracts, the max danger of the slender fly is $2475, and the max reward is $9400 – a few 3.8 reward-to-risk:

Delta: 0.46

Gamma: -0.02

Theta: 5.51

Vega: -77.86

Theta/Delta: 12

4 Ideas For Higher Iron Condors

The narrower fly has a greater reward-to-risk ratio.

The broader fly has a better theta, leading to an even bigger theta-to-delta ratio – each of which we wish.

With better theta, we additionally get bigger gamma (which we don’t need).

The expiration break-even factors are nearer (or narrower) within the slender fly.

The graph of the slender fly exhibits that they’re at $4950 and $5050.

These are the costs at which the expiration graph crosses the zero-profit horizontal axis.

Meaning the commerce needs to be worthwhile if SPX is between $4950 and $5050 at expiration.

Narrower break-even factors imply a narrower vary of profitability.

The break-even factors for the extensive fly are roughly $4930 and $5070.

This vary is wider by 40 factors, giving a wider vary of profitability.

The Narrower Fly Has Much less Capital At Danger. Is This The Cause Why It Has Much less Theta?

No.

On this instance, two contracts for the slender fly are nonetheless much less capital than these for the only giant fly.

Rightly so, the extra capital that’s within the commerce will present extra theta (with different issues being equal).

Nonetheless, that isn’t why the slender fly has much less theta.

Trying on the slender fly, we acquired 5.51 theta from $2475 capital of danger; this means that if now we have $3060 of danger as within the extensive fly, then math would say that we must always get 6.8 theta:

$3060 x 5.51 / $2475 = 6.8

Nonetheless, the empirical proof exhibits that the massive fly acquired 7.35 of theta – greater than what the slender fly would get even when we bump up the capital utilization of the slender fly to $3060.

There’s something inherent in regards to the wider fly that provides it extra theta.

Why Do Slender Flies Have Much less Theta Than Wider Flies?

The slender flies have the lengthy choices nearer to the quick choices.

It’s the quick choices which are giving us optimistic theta.

The lengthy choices have damaging theta.

The nearer the lengthy choices are to the quick choices, the extra the lengthy choices negate the optimistic theta results of the quick choices.

If we didn’t have the lengthy choices, we’d have a straddle that might give us extra theta than a butterfly on the similar strike and expiration.

On a per-contract foundation, wider flies use extra capital in danger than slender flies.

One can consider straddles as infinitely extensive butterflies.

They’ve limitless danger.

As a result of straddles are solely quick choices unhedged by any lengthy choices, they’ll generate giant quantities of theta.

That is additionally why wider flies can generate extra theta than narrower flies as a result of their lengthy choices don’t hedge their quick choices as a lot because the slender flies.

Slender flies look skinnier within the graphs and have a better reward-to-risk ratio. However that additionally means they’ve a decrease chance of revenue on account of narrower expiration break-even factors.

There are execs and cons to extensive and slender flies. Hope this text offers you a way of the traits of the 2 so you may decide one thing in between.

We hope you loved this text on the distinction between extensive vs slender butterflies.

If in case you have any questions, please ship an electronic mail or go away a remark under.

Commerce secure!

Disclaimer: The data above is for academic functions solely and shouldn’t be handled as funding recommendation. The technique offered wouldn’t be appropriate for traders who are usually not accustomed to change traded choices. Any readers on this technique ought to do their very own analysis and search recommendation from a licensed monetary adviser.