How Does the Passive Investing Impression Market Danger?

The rise of passive investing has been one of the vital profound tendencies within the asset administration business prior to now twenty years. Nevertheless, how does the recognition of passive funds impression market threat? We are able to depend on the info, and a current analysis paper exhibits that the impression is important, primarily by way of a considerable enhance in inventory correlations. As extra traders flock to passive funds, which monitor indices, the costs of shares inside these indices have a tendency to maneuver extra in tandem, growing market-wide threat.

The introduced paper focuses on the impression of passive investing on threat measures – second moments of inventory returns. Teachers discover that passive investing (and index-based frequent possession typically) has an uneven impression on completely different elements of threat: Whereas it contributes to systematic, co-movement-related threat measures, it’s primarily unrelated and infrequently noticed to be negatively associated to non-systematic, idiosyncratic actions. Since idiosyncratic value moments are thought of important indicators for firm-specific info, their discovering raises the query of whether or not the rise of passive investing (and different implicit index-based investing) will alter the knowledge construction and effectivity within the value discovery course of.

Teachers hypothesize and present that the recognition of passive investing can undo the advantages of diversification and result in greater market-level volatility: Market volatility has risen since round 2000 and is concurrent with passive investing, pushed by greater correlations amongst particular person shares.

A firm-level variable that captures the extent to which a inventory is held by passive funding autos – index funds and ETFs for the complete CRSP universe of shares, may be constructed. Authors discover a constant and sturdy outcome that this measure is very positively associated to threat measures that replicate a inventory’s co-movement with different shares and the market: its beta, its common correlation with all different shares, and its common covariance with all different shares, however it’s unrelated (and even negatively associated in some specs) to a inventory’s idiosyncratic volatility. In different phrases, a inventory’s publicity to passive investing positively contributes to the systematic (undiversifiable) portion of its threat however to not its non-systematic (diversifiable) portion.

Inspecting three episodes of sudden and largely exogenous rise in market volatility—the post-9/11 interval, the 2008 monetary disaster, and the 2020 COVID pandemic – in a difference-in-differences setting exhibits that the relation between passive investing and systematic threat turns into stronger throughout disaster durations as the chance contribution of shares with excessive publicity to passive investing will increase.

Correlated buying and selling by passive funds doubtless explains these results. First, shares extensively held by passive funds have greater buying and selling quantity (turnover) correlations with different shares. Second, the flow-induced buying and selling of passive funds contributes positively and considerably to the co-movement-related threat measures: beta, correlation, and covariance, however not idiosyncratic threat. These outcomes point out that correlated buying and selling impacts combination threat by way of a co-movement, or systematic, channel as a substitute of a volatility channel.

Whereas the research focuses on index funds and ETFs with an express passive mandate, the true extent of index-based investing could possibly be way more important on account of efficiency benchmarking and different fund supervisor incentives. Authors present that benchmark-driven closet-indexing practices have directionally the identical impact as passive investing on shares’ threat measures. Nonetheless, their results don’t subsume the impression of passive funds. Estimates recommend that express passive investing alone may clarify a 20% enhance in market threat over the past 4 many years (from 1980 to 2020). The true extent of the impact of index-based investing on market threat will, due to this fact, be much more important – doubtless double – if implicit indexing can also be thought of.

Authors: Lily H. Fang, Hao Jiang, Zheng Solar, Ximing Yin, and Lu Zheng

Title: Limits to Diversification: Passive Investing and Market Danger

Hyperlink: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4928631

Summary:

We present that the rise of passive investing results in greater correlations amongst shares and elevated market volatility, thereby limiting the good thing about diversification. The extent to which a inventory is held by passive funds (index mutual funds and ETFs) positively predicts its beta, correlation, and covariance with different shares, however not its idiosyncratic volatility. Throughout disaster durations, shares with excessive passive holdings contribute extra to market threat in comparison with earlier than the disaster. Correlated buying and selling by passive funds explains these outcomes, that are additional amplified by implicit indexing on account of efficiency benchmarking.

As at all times, we current a number of thrilling figures and tables:

Notable quotations from the tutorial analysis paper:

“[…] paradox is the main focus of our paper. We research how index-based investing – each index funds and index ETFs, which we collectively check with as “passive investing” on this paper – impacts the correlation construction between belongings and, finally, the general market volatility. Alongside the rationale outlined above, we hypothesize that passive investing will increase correlations amongst belongings and, since correlations amongst belongings decide the mixture market volatility, it additionally will increase total market volatility.Our speculation has profound implications for market effectivity and the associated fee and advantage of passive investing. A big literature exemplified by Jensen (1968) and Carhart (1997) has introduced sturdy proof of the advantages of passive investing: Actively managed mutual funds typically don’t outperform passive funds after charges and bills. However our speculation suggests an vital draw back to the numerous enlargement of passive investing: Its rise may result in greater market-level volatility, limiting the ability of diversification and the advantage of passive investing itself.

Our speculation relies on the notion that passive investing usually entails the simultaneous shopping for and promoting of securities inside an index, and this correlated buying and selling can result in will increase in shares’ systematic threat measures resembling beta and correlation with different shares (e.g., Basak and Pavlova 2013). To instantly make clear this mechanism, we first present that shares with a excessive index publicity have greater buying and selling quantity correlation with different shares available in the market. We then look at the impact of buying and selling induced by index and ETF fund flows (we name this passive-flow-induced buying and selling). We assemble a stock-level measure that captures the passive-flow-induced internet buying and selling of the inventory throughout all index funds and ETFs in our pattern. Presumably, the shopping for strain induced by the inflows of some funds could possibly be offset by the promoting strain pushed by the outflows from different funds. Our measure captures the web quantity of flow-induced buying and selling that can not be absorbed inside the index fund sector, thus displays a internet liquidity demand by index funds to different traders. We discover that this passive-flow-induced-trading is considerably correlated with shares’ beta, common correlation, and covariance with different shares, however negatively correlated with shares’ idiosyncratic volatility. Furthermore, the contributing results of passive-flow-induced-trading on beta, correlations, and covariance, are particularly sturdy in the course of the disaster durations outlined above. These outcomes assist set up correlated buying and selling amongst passive funds as a possible channel by way of which passive investing impacts market threat.

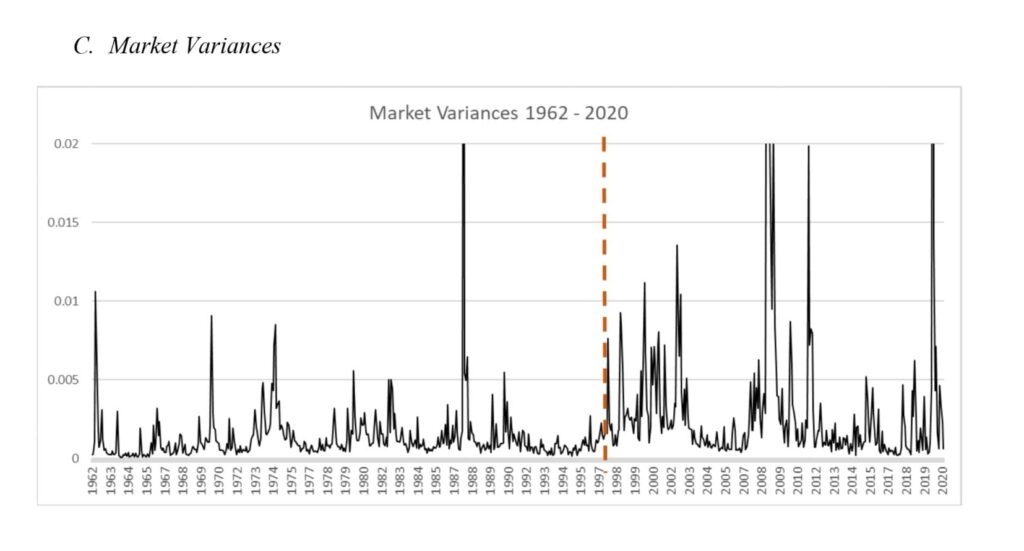

Determine 2 extends the pattern interval to 2020 and divulges a stark distinction between the pre- 1997 interval and the time since. Panel A exhibits that particular person inventory volatility continued to rise till about 2001 however has since declined. In distinction, Panel B exhibits a hanging enhance in pair-wise correlation amongst shares publish 1997: the common pair-wise correlation is 13.4% within the interval of 1998- 2020, greater than doubling the 5.7% for the interval 1962-1997 (t-statistic=17.85 for the distinction). Panel C exhibits that the web impact of those two forces is a rise in market-level variance within the publish 1997 period; the common pre- and post-1997 market annualized return volatility is 12.51% and 19.56% respectively, and the distinction is statistically important (t-statistic = 5.44).

[…] there may be a number of components contributing to the rise in correlations amongst shares, our paper focuses on the rise of passive investing—index funds and index ETFs. Determine 3 plots the extent of passive investing within the inventory market—measured by the “Passive-to-Market” ratio, which is the entire belongings beneath administration by index funds and index ETFs divided by the entire market capitalization of all shares—in opposition to the common pair-wise correlation amongst all shares within the CRSP universe over the interval of 1980 to 2020. Whereas the quarterly common inventory correlation sequence is kind of risky, the graph nonetheless reveals long run optimistic correlation between the 2 sequence.”

Are you on the lookout for extra methods to examine? Join our e-newsletter or go to our Weblog or Screener.

Do you wish to be taught extra about Quantpedia Premium service? Verify how Quantpedia works, our mission and Premium pricing provide.

Do you wish to be taught extra about Quantpedia Professional service? Verify its description, watch movies, assessment reporting capabilities and go to our pricing provide.

Are you on the lookout for historic knowledge or backtesting platforms? Verify our record of Algo Buying and selling Reductions.

Or comply with us on:

Fb Group, Fb Web page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookCheck with a good friend